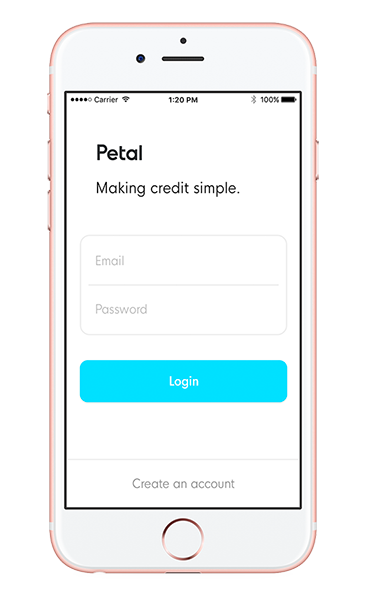

Petal gets $13 million to build a credit card for those without a credit history

You might be enjoying the benefits of a credit card with robust rewards today, but odds are when you were first getting started, it was hard to get even close to a card like that.

That’s because, for those just getting started or who have a poor credit history, those cards are generally out of reach — and a lot of them are, Petal co-founder Jason Gross said. That’s why he and his co-founders looked to start Petal, a service that identifies candidates that would be good credit card holders even if they don’t have a credit history, based on some of their actions rather than just their credit score. The startup said today that it has raised $13 million in a new financing round led by Valar Ventures.

“That has to do with critical changes in the market and access to do with credit post-financial crisis,” Gross said. “The way we think about credit scoring is sorely outdated, its tech was developed 60 years ago based on a limited subset of financial data that was the only info at the time. It disadvantages certain groups and society in particular. The data that you need to create a more comprehensive score is now available but not being used. When we assembled all those pieces, we felt this was a real problem for millions of people.”

Petal’s main product is a credit card, in which qualification for the card is based on the digital record it builds for its users. Rather than just looking at borrowing history, it looks at how much that user makes, spends or saves each month, and looks to offer them more differentiated products like lower interest rates on introductory products. The main goal here is to get people who should be able to responsibly manage a credit card, based on their spending history, actually get one in their hands and start building up that history.

A few of the startup’s most obvious targets are younger audiences that are picking up credit cards and associated products for the first time, as well as those who don’t have access to credit simply because they haven’t had an opportunity to build it. If you’re going to qualify for an important loan down the line — say, a mortgage — you need to build up that credit history, and that still requires actually getting in the door.

“If you look at folks who are thin-file, credit invisible, those who don’t have an accurate score, they’re predominantly young people but they’re disproportionately groups that have historically lacked access to financial services,” Gross said. “Minorities, immigrants, if you lack a score — or an accurate score — it can cost you very real money throughout your life. Having no score, you’re treated as subprime, you won’t qualify for most financial products, or they’ll be more expensive and inferior.”

Gross’ other hope is that the experience of using the Petal card itself (and managing it) will be a factor in convincing people to use it. One example he gave was the card telling owners explicitly how much of a balance they owe, and the amount of interest they will pay the following cycle based on what payment they are about to make.

There’s naturally a chance that, as people begin to build up a credit history thanks to Petal’s services, they’ll graduate into cards with more robust rewards like the Chase Sapphire line. Gross said Petal will still be able to offer something that’s a bit more differentiated than those cards, such as cards with higher limits or other kinds of benefits, and that it would still exist alongside those cards instead of its customers simply replacing it with something more rewards-oriented.

“We can grow with our customers,” Gross said. “We don’t have the same overhead as a Chase or a Bank of America. We’re not burdened by brick and mortar operations, we’re able to operate more efficiently. We can pass that value along to the customer. We’re able to underwrite or price credit risk that’s more accurate, and that allows us to lower the cost of credit. We can continue to offer our customers a compelling economic value proposition as they move through their financial life. That’s able to offer products with no fees, higher limits, over time being able to offer other sorts of benefits associated with the products.”

“We can grow with our customers,” Gross said. “We don’t have the same overhead as a Chase or a Bank of America. We’re not burdened by brick and mortar operations, we’re able to operate more efficiently. We can pass that value along to the customer. We’re able to underwrite or price credit risk that’s more accurate, and that allows us to lower the cost of credit. We can continue to offer our customers a compelling economic value proposition as they move through their financial life. That’s able to offer products with no fees, higher limits, over time being able to offer other sorts of benefits associated with the products.”

Petal isn’t alone in trying to identify good potential candidates for credit cards and getting one into their hands without a robust credit history. There are startups like Deserve, which raised $12 million in October earlier this year. Identifying these potential customers without a credit history is a tantalizing opportunity simply because the credit score might not be the best indicator, but it’s what banks and agencies have to work with for now. Gross hopes that Petal will be able to identify them with their technology and, by doing that, start to build up that big user base.

Featured Image: Rafe Swan/Getty Images

Published at Wed, 10 Jan 2018 15:00:32 +0000

{kind=link}